INTRODUCTION

Introduction

Lincoln County, North Carolina,

Tax Records

Kathy Gunter Sullivan, CGsm

Database History

First Phase, 1817-1840

In July 2007, Alta Mitchem Durden offered her collection of tax records to the Lincoln County NCGenWeb. Webmaster Derick S. Hartshorn promised space, volunteer transcribers were solicited, I consented to be project manager, and the project was born. Because of literally thousands of hours contributed by volunteers, researchers now have easy access to transcripts of 1817-1840 Lincoln County tax records. The original documents are available only at the North Carolina State Archives. Record losses in Lincoln’s parent counties -- Bladen, Anson, Mecklenburg, and Tryon – make these documents even more valuable.

Volunteer Transcribers

Bill Eddleman of Cape Girardeau, Missouri

Elizabeth Lankford of Charlotte, North Carolina

Kathy Gunter Sullivan of Charlotte, North Carolina

Jan E. Williams of Columbus, OhioSecond Phase, 1804-1806

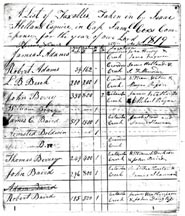

Robert C. Carpenter contributed his collection of 1804-1806 tax returns. In addition, he agreed to share his geographical knowledge of the districts’ locations, which provide valuable background context. Of the twenty-three tax districts in existence for this period, only these eleven returns are extant.

Third Phase, 1778-1795. Transcribing is underway.

Transcribers have donated their best efforts to reproduce these elderly, challenging, handwritten documents. Even so, the transcripts are a derivative source at least one step removed from the original. This does not make the reproductions unreliable, but it does mean the data have been filtered through the transcribers’ eyes. If a kinship conclusion hinges upon one of these records, then consulting the original at the North Carolina State Archives is well worth the peace of mind.

The goal, of course, is to create a database that is a reliable resource. Corrections or suggestions are welcome; direct those to Kathy Gunter Sullivan

Scope of Lincoln County Tax Records

Lincoln County tax documents at the North Carolina State Archives consist of a mixture of loose papers and bound volumes currently spanning the years 1784-1886. The records are not consecutive; they are a broken series. We have only eleven 1804-1806 tax returns for the period 1795-1815, even though the 1805 minute docket, for example, identifies twenty-three tax districts. Unfortunately, the Lincoln County minute dockets for part of April 1800 and all of July 1800 through July 1804 are not extant, leaving us with none of that information for the period’s tax districts. Adding to our misery of missing tax records and county court minutes is the fact that the pages of the 1810 Lincoln County census became disarranged before microfilming and present a confusing and inaccurate account of tax districts.

There is a publication available from Dr. Bruce Pruitt transcribing 1837 taxables from a bound volume (see http://members.tripod.com/abpruitt/). Although the State Archives filmed the county’s bound tax records for 1837, 1839-1845, 1854-1858 (microfilm C.060.70001), the film is mostly illegible. An accurate reading of those volumes requires viewing the originals.

Citing this Database

“Cite what you see” is fundamental to precise citation. A reader incorporating these transcriptions into a database as if he personally consulted the original at the North Carolina State Archives is not accurately citing this resource. To cite this database in general:

Lincoln County, North Carolina, Tax Records 1817-1840, online database at http://www.ncgenweb.us/lincoln/taxrec.htm : accessed [insert date]; citing Lincoln County Tax Lists, Box numbers CR.060.701.4-5, North Carolina State Archives.

A citation to a specific transcription should acknowledge the volunteer who contributed time and expertise to decipher the original. To cite a particular record in this database:

Lincoln County, North Carolina, Tax Records 1817-1840, online database at http://www.ncgenweb.us/lincoln/taxrec.htm : accessed [insert date], [insert record title and year], [insert volunteer’s name], transcriber; citing Lincoln County Tax Lists, Box number [insert number], North Carolina State Archives.

Tax Procedures and Laws

The county was arranged into administrative areas known as companies or districts called by the names of the elected militia captains. Company/district captains changed subject to annual elections; therefore, the names of the districts also changed. When population growth warranted, additional districts were created. In April usually, Lincoln’s court assigned a Justice of the Peace in each district to “take in taxes.” These appointments appear in the court minute dockets. My study confirms those assignments are not comprehensive lists of existing companies. In April 1821, there were twenty-one companies assigned to Justices, yet there are extant records for another eight companies not assigned in the minute docket. I have no explanation for these discrepancies. Still, the minute dockets of Lincoln County Court of Pleas and Quarter Sessions are useful for identifying most districts and very important for understanding their role in the hierarchy of county government.

The district constable rode his area “warning in” citizens to appear before the appropriate Justice, be sworn, and verbally report their taxable acreage, white and black polls, stud horses, jackasses, and stores. The Justices collected no money. The Clerk of Court received the justices’ tabulations, calculated the statistics, and made several copies (“duplicate made out & compared”). One copy stayed in the Clerk’s office, where taxpayers’ names were added to the juror pool (“freeholders taken off”). Another copy went to the Sheriff as it was under his supervision that tax money was collected. The final return to county court included adjustments for removeds (deletions for reasons such as moved, died, insolvent, and mistakes), and people failing to register (therefore liable for twice the tax rate). Tax income sustained the county and unapproved differences in the Sheriff’s return were his personal liability.

Do not assume that tax laws for a different time period or for another state apply universally. North Carolina’s laws evolved, and it is crucial to be aware of laws in effect during the particular period of your research. For the period 1801-1840, the following poll (head) taxes applied:

Free males between the ages of twenty-one to fifty years; revised in 1817 to twenty-one to forty-five years, and revised again in 1835 to twenty-one to forty-four years.

Slaves between the ages of twelve to fifty years; revised in 1835 to twelve to forty-nine years.

Free unmarried or widowed women were subject to real property (land) tax, but never to poll tax. If a woman appears with a poll on a tax record, then she has a male or a slave of taxable age in her household.

Study = Learn = Know

The authoritative resource for genealogical research in North Carolina is Helen F. M. Leary, editor, North Carolina Research (Raleigh: North Carolina Genealogical Society, 1996). Dedicated North Carolina researchers need this volume on hand for repeated study. For tax education, see “Strategies for Tax Records,” chapter 2, pp. 48-52, and “Tax and Fiscal Records,” chapter 14, pp. 230-239.

There is no quick way to search this database because of spelling variations and because people often appear under their agent’s name or within a neighbor’s property description. The names are written by the justices and are not evidence of the taxpayer’s spelling. Tip: names often appear in exact reverse order. A person recorded as Smith D. John should not be assumed to be named D. John Smith. More likely, his name is John D. Smith. Study the format of each document to grasp the context of its information. Even if your person of interest is not recorded, much can be learned by understanding tax procedures applicable to his place and time.

Golden nuggets in these records identify widows and their remarriages, heirs, sons, siblings, estates, administrators/executors, guardians, partnerships, stores, occupations, and financial situations, include physical or ethnic labels differentiating same-name people, and supply valuable signatures. Some taxpayers in these documents come of age and migrate away before ever appearing on a Lincoln County census.

Take the time to observe your target person’s neighbors because these are the people with whom he associates in a variety of circumstances. They may be in-laws or cousins, serve together on jury panels, participate in each other’s land surveys, witness each other’s deeds and wills, barter among themselves, sometimes attend the same church, migrate together to another state, and their children may marry. Collect events and associations from all resources, and record them in your target’s chronology. This methodology can reveal a person’s pattern of associations and movements as well as highlight impossible scenarios.

*Certified Genealogist (CG) is a service mark of the Board for Certification of Genealogists® conferred to associates who consistently meet ethical and competency standards. The BCG was founded in 1964 to promote excellence in research, teaching, writing, publishing, and librarianship by those who pursue genealogy as either a profession or avocation. The BCG website is http://www.bcgcertification.org.

Derick S. Hartshorn - ©2010-present

Last Modified: 06/22/2010 16:54:15